Discover more from HEALTH CARE un-covered

As Medicare Advantage's shortcomings echo in the press, key legislators still push to privatize traditional Medicare

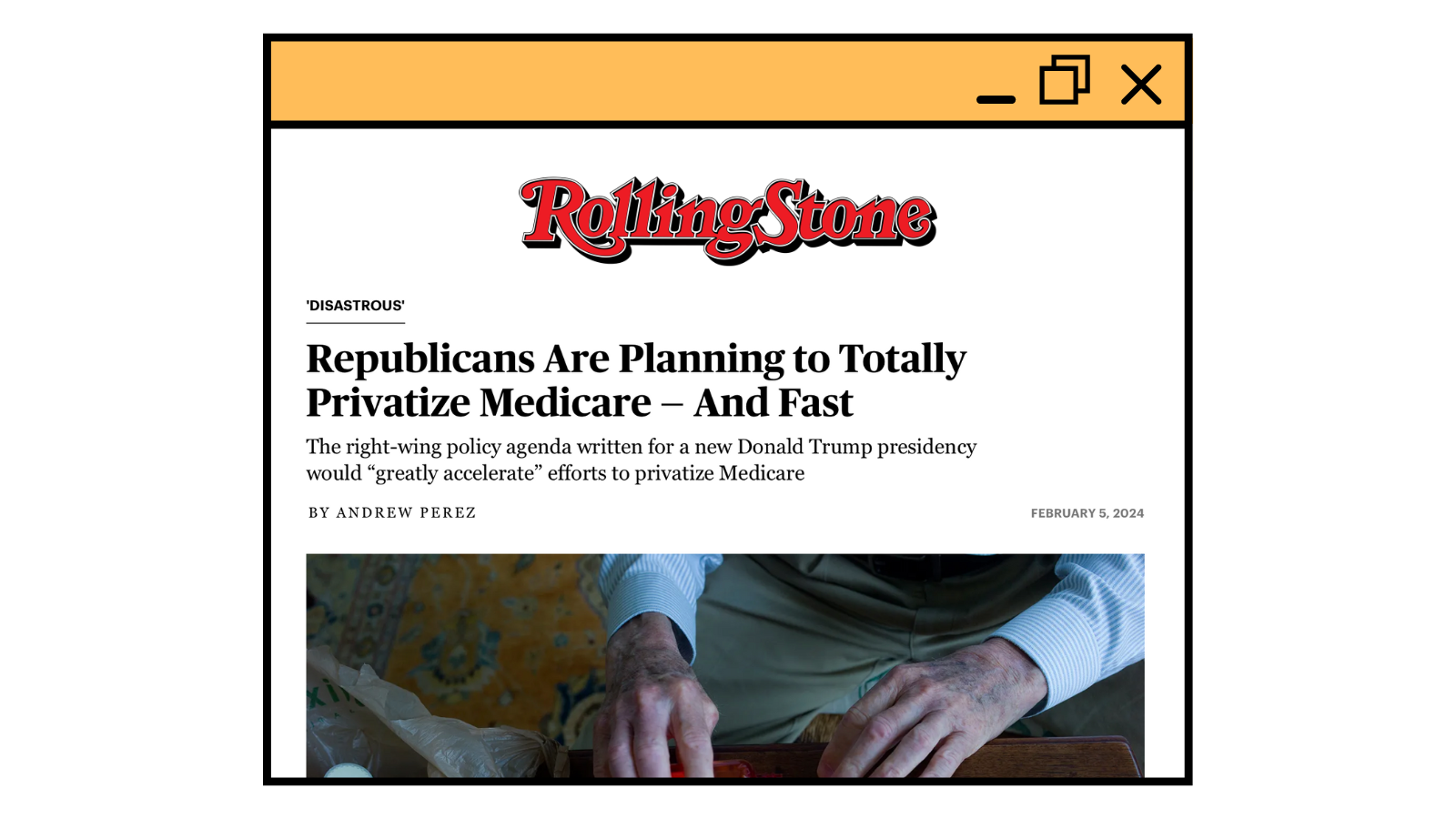

A story in Rolling Stone last month offered an ominous prediction about our nation’s health care. “The right-wing policy agenda written for a new Donald Trump presidency would ‘greatly accelerate’ efforts to privatize Medicare,” Andrew Perez wrote.

That story should be seen by the millions of seniors who might not read Rolling Stone but who have traditional Medicare coverage with a supplemental policy that pays for virtually every medical bill when they get sick. Those are the people who have not yet been enticed into Medicare Advantage plans with promises of groceries and gym memberships but with little or no notice about the delays in care and the up-front, out-of-pocket costs common in many plans.

As I pointed out in an earlier story, there are roadblocks to care that have been reported by hospitals that were no longer accepting Medicare Advantage plans from some companies. The CEO of the Brookings Hospital System in Brookings, South Dakota, was candid: MA plans “pay less, don’t follow medical policy, coverage, billing, and payment rules and procedures, and they are always trying to figure out how to deny payment for services,” he said.

Yet, in his piece titled “Republicans Are Planning to Totally Privatize Medicare – And Fast,” Perez warns that privatizing Medicare is a goal conservative and right-wing interests have promoted since the 1990s, when former House Speaker Newt Gingrich, no fan of Medicare, predicted that the program would “wither on the vine because we think people are voluntarily going to leave it.”

Indeed, tens of millions of seniors have enrolled in or been forced by their former employers into Medicare Advantage plans, and even the 30 million or so seniors who still prefer to be in traditional Medicare, with its no-strings-attached coverage, may one day be forced to join the ranks of the MA crowd.

It’s time to once again sound the alarm, as Perez has done, that the government program that has brought millions of beneficiaries health insurance and security for more than five decades could eventually disappear.

Perez points out that one item buried in the 887-page Heritage Foundation blueprint written to inform a potential new Trump administration has attracted little attention so far. It is a scheme to “make Medicare Advantage the default enrollment option” for people who are newly eligible for Medicare, he wrote.

David Lipschutz, associate director of the Center for Medicare Advocacy, says the Heritage plan would hasten privatization. “Upon becoming eligible for Medicare now everyone starts with traditional Medicare as the default but can opt out of that program and later choose an Advantage plan,” Lipschutz says. The Heritage proposal, however, would have people start with Medicare Advantage plans, apparently with the opportunity to opt-out. With this arrangement, you can see how easy it would be for Medicare, as we know it, to ‘wither on the vine’ since many people new to Medicare are not well versed in the difference between the two options and instead are swayed by the TV advertising beckoning them to Medicare Advantage plans.

Making those privately operated plans the default “would hasten the end of the traditional Medicare program as well as its foundational premise: that seniors can go to any doctor or provider they choose,” Perez writes, noting that such a change also “would be a boon for private health insurers that generate massive profits and growing portions of their revenues from Medicare Advantage plans.”

Lipschutz agreed the plan would “greatly accelerate” Medicare privatization, noting that the Heritage Foundation’s selling points are “internally inconsistent.” The proposal says a Republican-led federal government would “give beneficiaries direct control of how they spend Medicare dollars,” but Lipschutz pointed out that with a Medicare Advantage plan, a private insurer tells beneficiaries what procedures they can or cannot have by deciding which ones they will approve for payment. “That is the opposite of putting beneficiaries in control of how they spend their dollars,” Lipschutz says.

Stories in Stat by Bob Herman and Casey Ross have carefully dissected what patients with Medicare Advantage plans have had to endure to get needed care. As I pointed out in a post about their work, patients often struggle to get the care they need. In one story about UnitedHealthcare, the largest Medicare Advantage company, the reporters noted that the insurer’s stunning financial success was driven by “brazen behavior,” such as cutting off payments for seriously ill patients and “denying rehabilitation care for older and disabled Americans as profits soared.” UnitedHealth is far from alone in using such tactics to boost profits. Herman and Ross told of the struggle of a sick, 80-year-old North Carolina woman whose plan with Humana, the second largest Medicare Advantage company, would pay only for cheaper care in a nursing home instead of in a long-term acute-care facility.

The insurance industry’s mighty public relations machine makes it hard for ordinary Americans to understand their options when they turn 65. When a TV pitchman or woman is urging viewers to call right away and sign up for free groceries, the deck is stacked against traditional Medicare and supplemental coverage.

Meet the insurance industry’s “Better Medicare Alliance”

How many would-be beneficiaries know about the Better Medicare Alliance, an advocacy group promoting Medicare Advantage plans that swings into action at the slightest hint that lawmakers and regulators might curb the lucrative Medicare Advantage program? The organization’s website offered a sample letter for beneficiaries to send to their Congressional representatives urging them to “protect Medicare Advantage.”

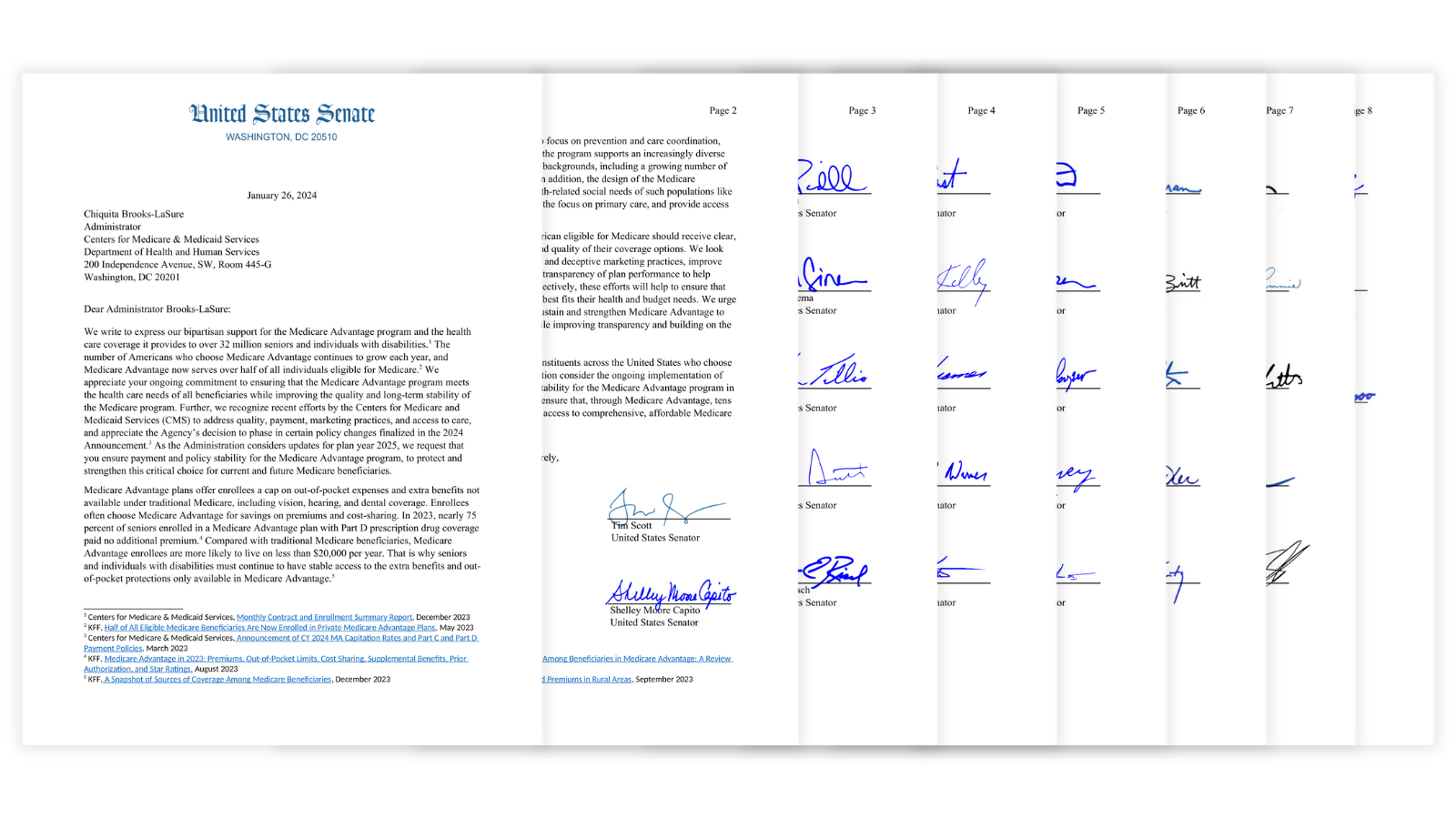

Sixty-one members of Congress also made their preferences clear in a letter to Chiquita Brooks-LaSure, who heads the Center for Medicare and Medicaid Services, writing, “We are committed to our more than 32 million constituents across the United States who choose Medicare Advantage.” The letter was signed by prominent Democrats including Chuck Schumer, Senate Majority leader from New York; Sen. Amy Klobuchar of Minnesota; and Bob Casey of Pennsylvania, who chairs the Senate aging committee. With such high-powered supporters of Medicare Advantage, it’s easy to see why it’s difficult to put the program on an even playing field with traditional Medicare and supplemental insurance coverage.

Not long ago I received an email from David Marans, an 81-year-old Floridian who wanted to tell me about his experiences with Medicare and the supplemental Medigap insurance he had purchased at age 65. It covers Parts A and B deductibles, excess charges that doctors can impose if their state allows them to collect more than what Medicare has agreed to pay, and emergency room care that he told me “ has saved considerable medical expenses, avoided delays, allayed worries, and allowed peace of mind regarding medical treatment.” He said he just shows his card at any hospital or doctor’s office, no questions asked, and the “Medigap provider then handles all the rest.”

The older you get, Marans said, the harder it is to recover from illness; the added stress of finding the means of paying the medical bills and the stresses of Medicare Advantage restrictions and denials can prolong illness. Marans said a Medigap plan alleviates that stress. “In a subtle way, in part, Medigap helps pay for itself.”

Marans’ advice? “Force yourself to get a Medigap plan on your 65th birthday when you enroll in Medicare, and don’t lose it… Seniors have to understand car insurance is for what might happen. Health insurance is for what very probably will happen.”

Subscribe to HEALTH CARE un-covered

Pulling back the curtains on how Big Health is hurting Americans and how we got to this point.

| A guest post by

|

And people don’t even realize that part c aka advantage plans are actually “for profit private insurance companies “and not Medicare.

Taxpayers are handing over at least $12,000 annually for each of the 32 million that are enticed to try part c. Part c profits could not exist without this blatant corporate welfare.

Please choose original/traditional Medicare.

These dollars need to go to providers and communities that actually take care of our health and not Wall Street.

It seems to me that many seniors choose "Medicare Advantage" Plans to avoid paying the 20% that Medicare doesn't cover. Medigap plans to cover this 20% are expensive and so Medicare Advantage Plans seem to be a cheaper alternative. Those of us in favor of single payer or Medicare for All should adopt eliminating the 20% medigap as a near term goal. It should slow the growth of so called "Medicare Advantage" plans and would be politically very popular